Property Investing is a Scam – Here’s Why It’s Not for Everyone

Is a property a good investment?

What I mean by investing in property is people who buy a property, then rent it out for a couple of years and the end goal is to sell it off after the price appreciates for a handsome profit.

From my observation & experience, undercon property investing is usually not profitable, especially for Millennials (Gen Y) & Gen Zs.

I will be using an undercon Malaysian property that I bought as a case study for this article, where I am experiencing a negative cash flow of RM 763 every month despite having a tenant to rent it out.

If you are a reader outside of Malaysia, the principles would be the same.

Here are the topics that I’ll cover in this article:

This article is NOT financial advice. I am sharing my opinions & experience. Please consult a financial planner.

What is an Undercon Property?

Buying an undercon property means you buy the property from the developer before or during it’s been built.

The biggest benefit to buying an undercon property is that you’ll get a brand-new home.

Here are the 3 common types of properties bought in Malaysia & their differences:

| Property Type | Meaning | Pros | Cons |

| Undercon | Buying from the developer before or during construction | – Brand new home – Little money down | – Oversupply – The developer can go bust during construction – A lot of marketing gimmicks |

| Subsale | Purchasing a completed home from an owner | You can see the house that you’re buying | It’s ‘used’ |

| Auction (lelong) | Purchasing a repossessed property from the bank | Sometimes cheaper than the other 2 | Must prepare a budget for repairs |

In the next sections, I’ll dive a little deeper into the pros & cons for an undercon property based on my experience:

Undercon Property Pros:

Let’s begin with the good stuff. The allure of a brand new property:

It’s a Brand New Home

There’s just something about a brand new property. From the smell of fresh paint on the walls to the electrical wires sticking out of the ceiling.

You get to pick out new lightings, furniture & kitchen appliances. It’s exciting to be part of the setup process & a chance to showcase your creativity.

Undercon Property is Cheap to Book

If you’re buying a subsale property, you’ll need to fork out 10% in downpayment + legal fees + stamp duties (let’s say another 3%).

So 13% of an average home price of RM 500,000 = RM65,000. That’s the amount you need in cold hard cash.

However, for most undercon properties, all of the mentioned costs are rolled into the selling price.

You’ll only have to pay the booking fee, which typically ranges from as low as RM 1,000 to RM 15,000.

A low booking fee to own a home is a great benefit for young couples about to start their life together.

Beware: The developer will claim that the legal fees are ‘free’ & ‘no downpayment’ but the reality is, all of these fees ends up in your mortgage, which you’ll be paying over the next 30 to 35 years. Jump to chapter: Marketing Gimmicks.

Undercon Property Cons:

The biggest drawback; you’re buying a property that doesn’t exist. You’re placing 100% trust in the developer that they will complete the project as promised.

The typical Malaysian high-rise build project will take between 3 to 5 years. During this period, here’s what can go wrong (worst case scenarios):

- The developer is dishonest and runs away with everyone’s money

- The developer goes bankrupt

- The completed property looks different than how it’s marketed

Nothing in life is guaranteed, including the developer’s ‘Guarantees.’ But what you can do to minimize risk on your end is to thoroughly research the developer and & their past project history.

Marketing Gimmicks: Cashback Is NOT Free Money

As the property oversupply situation worsens, unsold properties become a real problem for property developers.

Common ways developers put lipstick on a pig is through ‘cashback’ marketing gimmicks.

For example, an undercon property price is marketed at RM 500,000, and all buyers will get an RM50,000 cashback package.

Sounds attractive at first, think about it, how many years will it take you to save up RM50,000?

Think of all the possibilities that you can do with all that money:

- Withdraw as cash & spend as you wish

- Repay your loan (I doubt most people do this)

- Use the money to renovate your new home

The reality is that the developer increased the selling price of the property to include the ‘cashback.’

Cashback Is NOT Free Money

So that RM50,000 ‘cashback’ ends up in your mortgage.

So if you think about it, it’s almost like getting a personal loan for RM50,000 that you have to repay in the next 30 to 35 years!

I’d stay away from any undercon properties marketed with ‘cashback’ gimmicks.

You Have to Pay Progressive Payments Until Construction Completes

When you buy a regular house (subsale) at RM470,000, you’ll start repaying your monthly mortgage (around RM2,000) the moment the bank releases the money to the seller.

For an undercon property, it’s not that straightforward. The banks will release the money to the developer in stages according to the construction progress.

For example, 10% + 15% + 10% and so on until the developer gets 100% of the money from the bank.

Here’s an example of the loan release schedule based on the construction schedule:

You will have to pay interest for the disbursed loan amount that increases at each stage of the construction.

Depending on your bank, my interest payment started at around RM 70 a month.

Every few months, I’ll receive bank letters saying they have disbursed the following % to the developer, and the bank will charge me more interest.

The interest payment will keep increasing until 100% of the loan amount is released to the developer, at which I have to start paying the full monthly mortgage of RM 2,000.

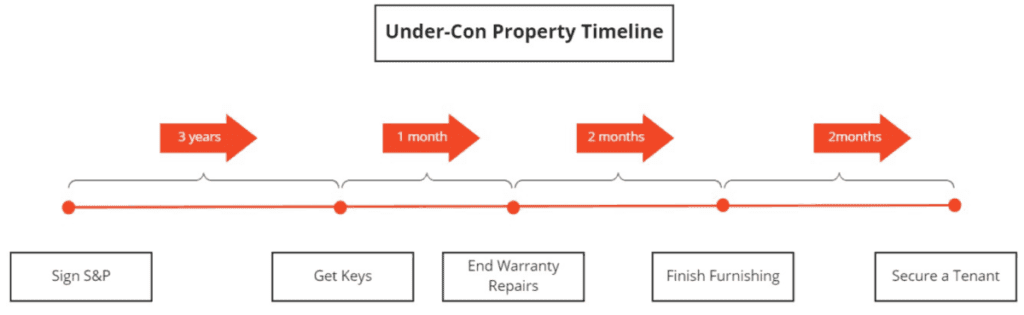

It took 3 years for the developer to complete the construction process. During which I can’t do anything to the property.

I can’t rent it out, can’t sell it. So I was stuck paying the monthly progressive interest and pray to dear god that the developer doesn’t run away with the money or go bankrupt.

Pretty scary stuff.

Checking for Defects While Still Under Warranty Period

After paying interest for 3 years, you finally got your keys! Hooray! There’s nothing more exciting than going to the developer’s office to collect your keys and entering your new property for the first time.

Even though most new homes have quality checks, many minor things will slip through, and you have to inspect and report any faults to the developer within your 1 or 2 year warranty period.

Some defects are easy to spot. Like shoddy paint jobs:

Some defects you’ll only realize at night, some only when you take a shower, and some only when you try to cook.

Even if this is an investment home, it’s a good idea to spend a couple of nights living in your new home to get a feel of the place.

For example, I had no idea that my walls were so uneven until I installed curtains and downlight from the ceiling:

Depending on the severity of your defects, it will take several back and forths with the building management to sort everything out.

Then, I invited a friend over, and he pointed out that my bedroom walls are crooked (not even).

Luckily he pointed that out!

I complained to the developer & they came again to fix it:

Paying Electricity Bill (TNB) Deposit as a New Owner

The new property owner will have to place an electricity deposit to TNB (the local power company).

Head on down to the nearest TNB office near your property to make the deposit payment. Mine was RM910 (USD 219), which caught me off guard a little at that time.

The deposit is shown on your TNB bills each month:

Furnishing the Apartment Costs Money & Time

After everything is fixed and cleaned up, it’s time to install lights, ceiling fans, curtains & some furniture so it’s attractive for tenants to stay in.

It cost me RM 10,193 (USD 2,405) to fully furnish my 1-bedroom apartment.

Here are some photos I took during the setup process:

Expect several trips to the lamp store, IKEA, and furniture stores. Do not underestimate the amount of time and energy needed to furnish your new property. It can take up another 1 to 2 months to complete.

Some furniture stores will also have backorders and delivery schedules, which will delay your home’s furnishings even more.

You also have to take measurements to custom order curtains using a measuring tape. My living area window is two stories tall. I had to get the curtain guy to come in and measure the height using a laser tool:

From my observation, most landlords put minimal effort and money into furnishing their properties. So it doesn’t take much effort for you to one-up your competition.

Put yourself in the shoes of a tenant. What would make your apartment unique compared to the rest?

If you’re targeting a family, furnish your property to appeal to the wife during viewings. My secret sauce that usually works is:

- Include option for free WiFi

- Buy an oven

- Get a 2 door fridge

- Washing machine + dryer

- Paint a featured wall

- Include some carpets & floor mats

- Place some robust house plants

With a few interior decor ideas from Pinterest & Instagram, you can easily distinguish yourself from the pack while keeping a low budget.

Here’s my results:

Featured Wall: I picked a color & painted a featured wall to bring some life to a bland white living room. The total cost to buy paint & brushes was only RM 60 (USD 14). The time it took me to paint by myself: 2 hours.

Total Setup Cost: MYR 10,193 (USD 2,405)

Massive Competition to Find Tenant Upon Handover

Great, the place is all set up, it’s time to find a tenant to help you pay your mortgage. Unfortunately, that’s exactly what the owners are doing too. They all want to rent it out as soon as possible, for as much as possible, just like you.

Can you rent your place out at the same price or more than your mortgage (RM 2,000)? The only way to figure that out is to check the market price online. Some popular websites you can check are:

Putting yourself in the shoes of the tenant, they are shopping around for the best deal. They know that all of the owners just got their keys and are all competing for a tenant. The ball is in the tenants’ court.

The longer the apartment is left unrented, more and more owners start to lower their prices, bringing the average market rental down. After a few months, the average rental is now RM 1,700.

After a few price readjustments, viewings, and negotiations through your agent, you secured yourself a tenant! Yay! Final rental price: RM 1,600.

Alright, not ideal, you’re at a deficit each month of RM RM 1,600 – 2,000 = -RM 400.

But it gets worst. Let’s not forget all the other bills that the owner (that’s you cutie pie) has to pay:

- The property agent’s one-month fee.

- The management maintenance fees (usually free for a year or two).

- Quit Rent (cukai pintu).

Phew, that’s a lot of stuff, no one will ever tell you about all of these before you sign that Purchase Agreement.

Let’s whip out a calculator and table spreadsheet to calculate our monthly loss:

Calculating Negative Cashflow

Property Agent: Their fee is usually 1 month of rental + any taxes + stamp duties.

Management Maintenance Fees: These are the fees that the building management collects from all owners to pay for their salaries, maintenance of elevators, general upkeep, and security personnel.

Typically (but not always), developers pay the maintenance fees for owners for the first one or two years.

Cashflow bleed:

| Reality Check | Monthly | Yearly |

| Mortgage | -2,000 | |

| Agent Fees | -141 | -2,250 |

| Maintenance Fees | -180 | |

| Quit Rent | -42 | -500 |

| Rented out for | 1,600 | |

| Profit or Loss | -RM 763 |

According to this table, you’re at a RM 763 deficit each month. In a year, that adds up to RM 9,156!

You need to rent out your property at RM 2,763 to break even.

It’s going to be tough because RM 2,000 is already at the edge of what most Malaysians can afford to rent.

Let’s recap your loses: 2 months of full mortgage payments during the setup process; RM 4,000 + RM 10,000 (setup cost) = You’re currently down RM 14,000.

Undercon property doesn’t seem to be like such a good investment now is it?

Light at the End of the Tunnel

So what now? How can you recoup your money back? I am no expert, but I can only see 3 ways:

- Hope that the area and property become more populated (demand > supply) so you can raise the rental price.

- Hope that after many years, the market value of the property increases, and you’re able to sell it more than your accumulated deficit.

- If all fails, you can stay in your under property while you wait for the above to happen.

Below is the timeline:

This is my experience. I bet there are people out there that are making money through property investments. But for most people starting, I think they’d be in a similar boat as me.

Undercon Property Investing Summary:

The property prices have inflated far more rapidly than the increase in the Malaysian average salary. In short, there are too many expensive properties, but not enough Malaysians who can afford to buy them.

Investing in property is old advice that used to work for Baby Boomers & Gen X during their time. Unfortunately, advice that works in the 1980s & 1990s doesn’t work anymore in 2021.

Only buy a normal home (3 bedroom at least) for your own stay.

In hindsight, here’s what I would do instead of buying this undercon property:

- Buy an auctioned property. It might be a good idea to network with people who’ve already done it.

- Buy property during a recession (like during a global pandemic).

- Invest in REIT’s instead, which is like stocks, but for properties. You can check out Marcus’s guide on REITs.

Investing in robo-advisors would make much more sense for most people. You can read my Wahed Invest review here. Use my referral code mohhas198 to get FREE RM10 in your account.

Do share with me in the comments if you have any interesting stories of your property investment journey!

Thanks Helmi.

Very well written and more importantly, provides a balanced view rather than “it’s all rosy picture” for those looking for guidance in property investment. Keep it up

Thanks for the kind words Eddie

Hey, I saw a link to this article posted by Ringgit Oh Ringgit on Facebook. I’m so glad I clicked on this!

This was a fantastic write-up/breakdown which was really insightful, because as you’ve correctly pointed out, this sorta stuff on the “other side” is certainly not revealed when you’re speaking to property developers/agents who are just trying to get a sale! I really liked your use of diagrams, tables and photos too!

On your final 4 points, I am a bit curious about point 2, but I say this without having done any real research as to the impact of the pandemic on both property prices and rental. My gut feel is that, whilst, yes, developers will also be looking to offload property at a lower price, the rental market will also be affected. Not forgetting that this pandemic has had market-wide implications, and I imagine if there is an impact on the property market, it should affect both the value of property, and the expected rent you should be able to command as well.

On point 1, why do you think an auctioned property might be a better choice? Are you referring to buying from an auction where you hopefully are able to pick up a property at below market value? Would there not be a risk though that the seller’s reserve price is still too high for your liking, and this reserve price is likely to be at, or close to market value anyway?

Thanks for your comment and support Wayne, I am looking into an Auctioned property for the next purchase. That being said, thorough research needed to be done to make sure that it is significantly cheaper than sub-sale. An auction property can be cheap, but it can come with its own headache. I will seek advice from friends who have done it before I venture into this. I will write about it when the time comes.

Dear Helmi,

Thank you for the well-thought given piece of writing. As I read through the post, it hits so me with so many “yeah, exactly what I thought” and “i knew it!”. Much of my assumptions were pretty much similar to your key points.

I started working about less than 3 years ago after such a long “education“ journey and I was really excited about properties and interior decor. Since I was a child, my family always rented in a simple modest home. My late dad was never much into property, Never felt making the house pretty, homey and such. We just lived they way we could within that house. So, I wanted to make my life a different one once I have my own money.

I visited many sub con open days, showing galleries. At one point, I almost, almost pen down a unit, like you said, a low entry, low booking fees to a 450~500k 2 bedroom apartment. But then I held back and keep going around. From all these visits, I found the same pattern from all developers. Rebates under the name of HOC, low entry booking fees, other fees waived, and also furnitures. The first one about HOC is to me, the most taken advantage leverage taken by those developers. They offset these discount buy raking up the total price of the property. At the end, yes the newly proud owner having to pay the humongous fees in interest down the line. Developers are doing what they think gives them maximum “untung” without realising how much these will affect the economy as a whole. We are screwing our young generations simply said as that.

As for rented units, I am too looking for one as I’m planning to get married soon. Your point on owners care so little about furnishings is 100%. This is very true for newly completed units. Owners seem to have an idea that their units will get rented unfurnished~ Bare sinks, no lightings installed yet etc. No renter would go and trouble themselves to build a kitchen cabinet, install lightings, curtains, buy a fridge, washing machine. These are all basics for a living. All those basic items will cost renter easily 10k. Spread out over a year, almost 1k each month on top of the rent. Don’t forget about bed and cupboards in the bedroom. So all these, would not make sense to a renter especially if they might move out after 1-2 years of renting. Owners are just limiting their own chances in this “investment”.

I hope Malaysians can get more exposure to real estate industry. It’s a wonderful industry to begin with, as everyone needs a home. I envy those countries like US, Europe. They have so much options and varieties. So much ideas and designs in a home. Whereas what we see in Malaysia today, 80-90% of apartment having the same layouts, same design and over estimated future value handed to these poor owners.

We need more people like you to educate Malaysians on being real estate savvy people. Again, thank you for the writing. Cheers and have a good day.

Hi Dharmiry

congratulations on the longest comment on this blog! I’m happy that my writing resonated with you and thank you for your kind compliments 🙂 More keeping-it-real articles coming up!

Hi Helmi.

Thank you for sharing your view. I live in Seremban. I haven’t had any property yet and im thinking into buying one but looking at the price of a new developing house, I started to think it’s more worth to buy a subsale property rather than from the developer’s. In my opinion, a subsale property area is more likely developed compared to the new house area. More shops, easy access to public transportation, malls, mosque etc. Although the price range is not that different than the new developing house but it can get you save too. Let say the subsale property for a one single terrace house here is RM 220k, it can save you arounf 5k-10k from buying from the developer. But your house might not be too new la plus you need to fork out your savings into paying legal fees, stamp duty and deposit not including the renovation you might want to do.

p/s: I love reading your thoughts and views. Thank you for sharing views from good and bad perspective in your articles!

Thank you for your kind comments!

I think we all need to trust ourselves when making a decision and not blindly follow what everyone is doing because it is the ‘norm’.

Btw, so cheap houses in s

Seremban! But the commute would kill me so I can’t do it

I, too, was caught in the whole “first property investment” hype that encapsulated the country from 2010 to 2014. Bought my first property in 2014 while it was still in development but missed out on the LDP, which most of my other neighbors managed to get! For them, it was a win-win. They bought it a much cheaper price in 2011 and because the place was completed 5 years behind schedule, they managed to get some money from the developer. Unfortunately, I bought this during the housing bubble, so didn’t get to enjoy the payout.

Even though my unit has managed to get tenants over the past years, it is a hassle trying to ensure your property doesn’t blow up while under your tenant’s care. And since my unit is in Cyberjaya, most of the tenants are students so the search for the next tenant is never ending. Am not even going to get into the amount of money I’ve invested in this place already….so yeah for all those millennials who’re looking for investment property, consider spending your money on other investments. The undercon property market is overhyped…perhaps I’ll also look into auctioned properties or subcon property next time as well.

Oops, sorry that was Late Payment Interest instead of LDP. 🙂

Totally,

Property investing is totally Boomer advice in my humble opinion 🙁

Hi! I have a question on the interest payment during construction.. does this mean that all those money paid during construction is “burned”? If I buy a property undercon 5 years to completion vs 1 year to completion, the latter would waste less money?

No money is burned. You’re paying interest on the loan that you applied for. The banks will release the loan amount (under your name) to the developer in stages of construction. I don’t think one scenario will be financially better than the other.

Ah, brings me back to the days where I wait anxiously for my apartment to be completed, hoping that the developer doesn’t run away and abandon the project lol. I do not think I ever want to relive that lol. I was fortunate to have invested in the property during times when it was still affordable. I really feel for Gen Z and Millenials. Everyone should have access to affordable homes :/ That said, I hope that what you wrote here discourages people from buying property for the sake of investing, because honestly, it doesn’t seem worth it anymore. Hopefully then can the market cool down. Somewhat.

I am also trapped in 2 properties at the moment with no light at the end of the tunnel. Wish me luck!