Don’t Get Ripped Off – I Bought Insurance through a Financial Adviser

I hate that my previous insurance agents ripped me off (or more like took advantage of my naiveness).

I was paying for expensive insurance with low coverage.

Now, at 35 years of age, I’ve finally bought ‘decent’ life & medical insurance for myself & my newborn son.

But my insurance journey was not smooth:

- I initially bought expensive insurance with low coverage.

- Something forced me to terminate my insurance.

- Once I was ready to re-buy insurance, I find it hard to get high-coverage insurance with low monthly payments.

- I keep getting insurance agents who pushed insurance products I don’t need.

- How I finally am happy with insurance coverage within my budget.

This topic did so well, that my tweet got over 500k impressions:

So I know this is a great topic to write to share my insurance journey & help other people:

- Who is considering buying insurance but don’t know which to get & from who?

- People who already have insurance but considering getting a better deal.

Let’s start with how I bought my 1st insurance:

I Bought Insurance I Had No Clue About

When I started working after graduating in 2010, everyone recommended me to buy insurance.

It’s the next logical ‘adult thing’ to do.

So I asked them for their insurance agent contacts, and I set up an appointment with them at a nearby Papparich (remember those?).

I met two insurance agents, one from Great Eastern and another from Prudential.

If I’m honest, the insurance coverage and the monthly payment are similar.

I couldn’t tell the difference without scrutinising each insurance policy, which is impossible for the average Joe to understand.

I couldn’t recall the full details of my insurance policy, but here’s roughly what I can remember:

| Insurance Details | RM |

| Monthly Payment | RM 300 |

| Life & Disability Insurance Coverage | RM 150,000 |

| Critical Illness Coverage | RM 100,000 |

| Medical Card | I don’t remember the annual limit |

Looking back at my life insurance coverage, my next of kin will only get RM 150,000 (USD 34,400) if I die. Are you serious?

Let me put in perspective how low RM 150,000 insurance payment is:

- RM 150,000 can barely buy a new Honda Civic.

- RM 150,000 can’t settle a RM 500,000 outstanding average mortgage.

- RM 150,000 can barely pay for my child’s local private education. Forget about overseas.

My insurance coverage was low because the insurance agent sold me an investment-linked insurance policy.

About half of my RM 300 monthly payment goes to a mutual fund investment scheme.

So my insurance contribution is less than RM150 each month, which explains the low coverage.

But I was young, and I wasn’t concerned about death.

So I just went with it.

What Made Me Cancel My Insurance

During the 2020 COVID pandemic, my Airbnb business tanked.

Like many businesses during that time, I suddenly had no income.

I messaged my insurance agent to terminate & surrender my insurance policy.

I got back some money from the investment part of that insurance policy & was able to cover my expenses for a couple of months (I guess investment-linked insurance is not all bad).

I then tried to figure out what to do for money mid-lockdown.

That’s when I started this blog & coincidentally, my career as a Content Creator.

I soon had a decent-paying job as a Content Marketer in a local tech company & I got married in 2020.

In 2022, my son Zachary was born & I wanted new insurance to cover me & my son.

Insurance Definitions in Layman Terms

Here’s the insurance that I think I need, explained in layman’s terms:

| Insurance to Consider | Definition | For Myself | For my Son |

| Life or Disability | Lump sum payment to next of kin if you die or are permanently disabled within the policy period. |  | |

| Critical Illness | Lump sum payment to cover living expenses if you’re diagnosed with cancer for example. | | |

| Medical Card | It will pay all/part of your hospitalization bills up to the coverage amount. | | |

| Personal Accident | Disability or death due to an accident, not an illness. | |

My son doesn’t have any mortgage payments, so I feel he does not need life insurance.

I am primarily concerned about hospital bills. So the minimum coverage I want for my family is a medical card.

Researching Insurance Online

I started researching insurance online & I wanted to understand the policies myself without having to meet an agent.

So I only considered insurance companies with good UI/UX website designs & minimal insurance lingo.

Some insurance companies that I looked at were:

| Insurance Company | Pros | Cons |

| Etiqa | Simple website & easy to understand (no lingo). You can buy most insurance products directly online. | Too many products and I need help choosing the best insurance product. |

| AIA | Good looking website. | I can’t buy insurance on their website & need to contact their agent (which is what I don’t want to do). |

| FWD | The best insurance website I’ve ever seen. Can give me an instant quote. | Some Insurance products I can buy online, some I need to contact their agent. |

| Allianz | Clean website. | Too many insurance products to choose for myself. Still need to meet their agent to purchase. |

The other well-known insurance companies, such as Prudential & Great Eastern had terrible website user experiences as they’re riddled with insurance lingo.

Of all the companies I’ve researched online, I liked FWD’s website the best. It’s modern and fresh & the copywriting is simple to understand.

Unfortunately, despite all the information available online, I got overwhelmed during my research & understand that I can’t run away from meeting an agent.

Meeting the Insurance Agents

The following are my experiences. Your experience may vary.

| Insurance Agent Company | What I Like | What I Don’t Like |

| FWD | Knowledgable agent & a nice person. | The agent told me that FWD doesn’t have family medical cards or coverages for babies, which is weird & a deal breaker. |

| AIA | Online meeting. | Typical insurance agent. Keeps pushing investment-linked, which I don’t want. |

| Allianz | Nothing | Typical insurance agent. Keeps pushing investment-linked, which I don’t want. |

Out of all 3 agents that I’ve met, the FWD agent was the one I was most happy with.

The meeting was good, the pricing was within my budget & the quotation was easy to understand (for the most part).

For some reason though, the agent told me that there is no medical coverage insurance product for babies.

It was hard to believe & that was a deal-breaker.

So back to square one.

Meeting with a Financial Adviser

I was chatting with some friends in one of my WhatsApp groups & someone brought up that one of our lads worked as a financial adviser.

A quick background check of his online presence, and I was convinced this guy is legit.

I scheduled an appointment with him at my home.

What is a Financial Adviser?

Financial advisors are a “one-stop-shop” by providing everything from portfolio management to insurance products. They need to be registered & have relevant license in order to give out financial advice to their clients.

Investopedia

Without boring you to death, the main difference between Financial Advisers & insurance agents is:

| Insurance Agent | Financial Adviser |

| Tied to 1 insurance company & suggests insurance products from that company only, even though they may not fit what I want. | Work with several insurance companies & can mix & match insurance products from multiple companies to fit my needs & budget. |

How the Financial Adviser Tailored My Insurance

The Financial Adviser can give you better recommendations if you have some idea of what you want or don’t want.

This is what I told the Financial Adviser for him to better recommend me a fitting insurance plan:

- I don’t want investment-linked insurance.

- I want insurance for me & my son, as shown in the table above.

- My monthly budget for all of my insurance is less than RM500.

- I want him to propose better insurance than the quotation from FWD.

With these specific inputs, he worked his magic & came back to me 1 day later with 3 proposals.

The Financial Adviser’s Insurance Proposals

For the Medical Cards:

| Medical Card Details | Price |

| My Monthly Payment | RM 170 for me (I’m 35 during the application) |

| Son’s Monthly Payment | RM 150 for my son |

| Annual Limit | RM 1.25 million each |

| Lifetime Limit | No limit |

I was pretty happy with the medical card, which was a Takaful product from a local bank.

Next, we take a look at some extra coverage for myself:

- Life & permanent disability

- Critical Illness

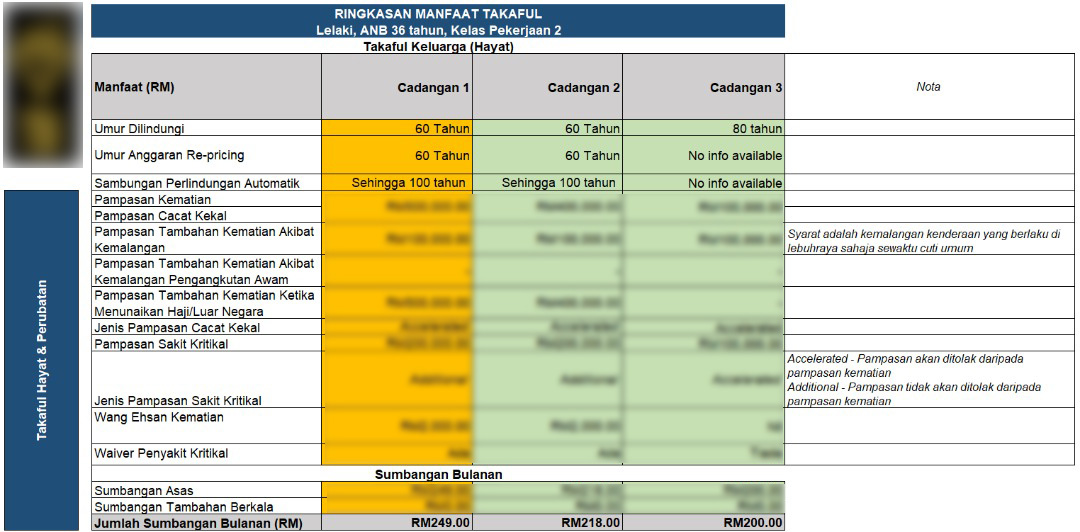

The agent WhatsApped me 2 proposals, with the column highlighted in yellow being the best out of the three:

I was pretty happy with the coverage & price, & we met one final time at my home to seal the deal.

My Son’s 1st Medical Claim

One day, we placed our son on the sofa temporarily.

It so happened that it was the time that he learned how to turn his body, and fell off the sofa & hit his head on the floor.

Being first-time parents, we panicked.

The baby was crying badly but calmed down after we soothed him.

Then we called our paediatrician & drove to the hospital.

I registered at the counter & showed the baby’s medical card. The policy that we had did not require us to pay anything upfront.

The paediatrician did some checks & a scan.

Luckily, the conclusion is that the baby is fine.

Since the incident is considered an accident & the baby was not admitted, I can pay first & claim back the receipt from our insurance through our Financial Adviser.

The claim process took approx 1 month to be approved:

Here’s proof that the money was indeed transferred into my bank account:

Not bad!

This also shows how important it is to have a credit card to help pay for emergencies first.

My Key Takeaway

Stop getting ripped off by selfish insurance agents (not all, but many are).

Nobody’s perfect & Financial Advisers are also working for a commission.

But from my experience, FA’s are the lesser evil of the two.

Connect with My Financial Adviser

I would be happy to connect you with my Financial Adviser to get you & your family covered.

Please fill out the form below & he will contact you to set up an appointment.

If you’re facing any issues with the form, please submit your answers manually to: helmi@helmihasan.com.

![[Save on Coffee]: Should You Buy an Espresso Machine or a French Press?](https://helmihasan.com/wp-content/uploads/2021/06/Blog-1-768x512.png)

![[Survey]: Average Malay Wedding Cost Breakdown – Guide for Couples](https://helmihasan.com/wp-content/uploads/2022/05/WEdding-cost-survey-768x512.jpg)

I’m interested especially on the advice from financial adviser

Hi Zuhairi, make sure you fill out the form at the bottom of that blog post

FWD Takaful got medical card for family include baby. Maybe that agent not knowing all product offered by FWD